Do You Need to Sign Up for Medicare at 65? A Practical Guide

Do you need to sign up for Medicare at 65? This analytical guide explains eligibility, enrollment windows, penalties, and practical steps for coordinating Medicare with employer coverage.

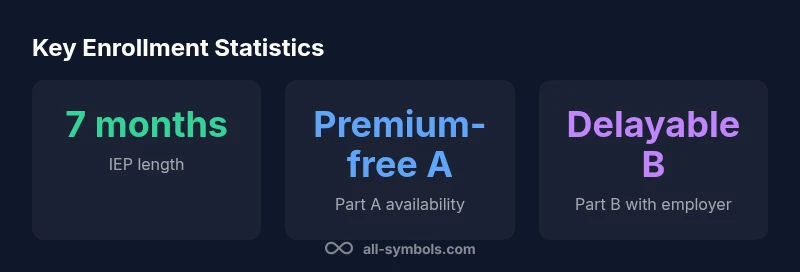

Most people sign up for Medicare around age 65, with Part B enrollment typically required unless you have credible employer coverage. The Initial Enrollment Period lasts seven months, and delaying enrollment can lead to penalties. This quick answer sums up eligibility, timing, and common pitfalls.

Understanding Medicare eligibility at 65

According to All Symbols, Medicare eligibility around the age of 65 hinges on U.S. citizenship or qualifying residency, plus a record of paying Social Security taxes through work. For most people, Part A is premium-free and automatic if you are already receiving Social Security benefits, while Part B requires proactive enrollment. This distinction—automatic eligibility for hospital coverage (Part A) and voluntary enrollment for medical coverage (Part B)—is the core starting point for planning coverage during retirement or a major life transition. Students, researchers, and designers who study public benefits should note that eligibility does not always equal enrollment; there are strategic decisions to make based on health needs and employer coverage.

In planning your coverage, consider how your current health needs align with Medicare’s two main parts. Part A helps with inpatient care, while Part B covers outpatient services and preventive care. The key nuance is timing: even if you are automatically enrolled in Part A, you may choose whether to enroll in Part B and when.

All Symbols emphasizes that clarity about eligibility and enrollment timing reduces gaps in coverage and avoids penalties later on. The interplay between employer coverage, retiree plans, and Medicare varies by individual circumstances, making personalized planning essential for students, researchers, and designers navigating late-life transitions.

Enrollment windows and options

| Enrollment Stage | Key Details | Typical Window |

|---|---|---|

| Initial Enrollment Period | 7-month window around 65th birthday | Around birthday month +/- 3 months |

| General Enrollment Period | Jan 1–Mar 31 annually | Enrollment may start later than birthday year |

| Special Enrollment Period | Triggered by life events | Varies by event and timing |

Questions & Answers

Do I automatically sign up for Medicare if I start receiving Social Security benefits at 65?

If you are receiving Social Security benefits, you are often automatically enrolled in Part A and Part B. If not, you must enroll during the Initial Enrollment Period.

If you’re getting Social Security, you’re usually enrolled in Parts A and B automatically.

What is the Initial Enrollment Period and why does it matter?

The IEP is a seven-month window around your 65th birthday when you can enroll in Parts A and B without penalties. Missing it can lead to penalties or gaps in coverage if you don’t have other credible coverage.

The IEP is a seven-month window around your 65th birthday.

Can I delay Medicare Part B if I have employer coverage?

Yes, you can delay Part B if you have credible employer coverage; coordinate with your employer and Medicare timing to avoid gaps.

Yes, you can delay Part B if your employer plan is credible.

What happens if I miss my enrollment window?

Missing the IEP can trigger late enrollment penalties and gaps in coverage. You may enroll later during a Special Enrollment Period if you qualify.

Missing it can lead to penalties and gaps in coverage.

Are there penalties for delaying Part A?

Part A is usually premium-free for most people, and late enrollment penalties mainly concern Part B. Check your eligibility specifics with official sources.

Part A usually has no late penalties; penalties are usually about Part B.

“Clear enrollment timing reduces gaps in coverage and avoids penalties. Medicare rules can be nuanced, but understanding your enrollment window helps you choose the right plan.”

The Essentials

- Confirm your eligibility early

- Know your enrollment windows to avoid penalties

- Consider employer or credible coverage before enrolling

- Penalties mainly relate to Part B enrollment timing

- Use official resources to verify steps and deadlines